The critical question is not simply whether employment increased —

but who truly benefits from that increase.

In this analysis, we will focus on understanding the latest unemployment report, where we appear to be entering a period of stability in the labor market, with 130,000 jobs reported for the month of January 2026 and a cooling in the unemployment rate of 0.1%, bringing it to 4.3%, very close to the Federal Reserve’s target of 4%.

A single unemployment rate can suggest broad stability. But a labor market is not a single organism; it is a composition of demographic and industrial segments. When we disaggregate the data by age, race, and industry, including sectors such as financial services, we move from abstraction to structure. The purpose is not to presume imbalance, but to observe distribution. If employment gains are truly broad based, that breadth should be visible across categories. If not, the concentration itself becomes analytically meaningful. The data allows us to see. Our task is to interpret.

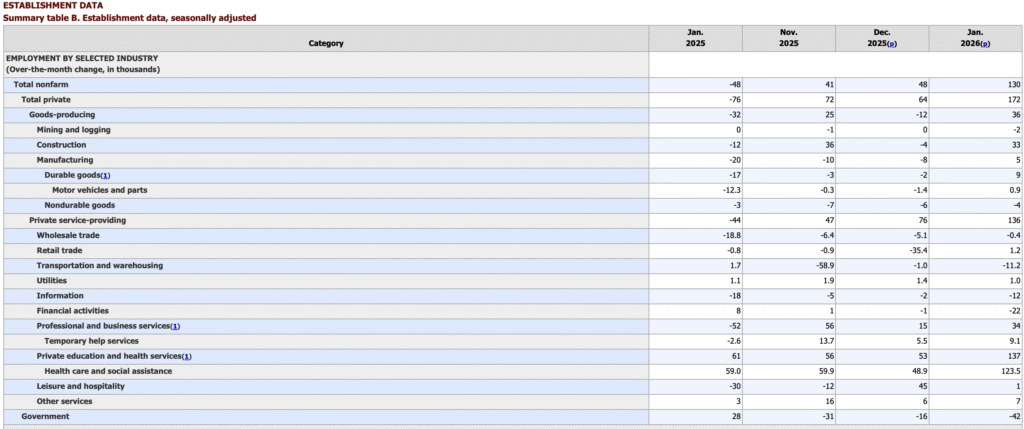

The table above, drawn from the Bureau of Labor Statistics Establishment Survey, breaks employment growth down by industry, allowing us to see not just how many jobs were created, but where they emerged. In January 2026, total nonfarm employment increased by 130,000 jobs. Yet private education and health services alone accounted for 137,000 of those positions, more than the entire net gain for the month. This means that the overall expansion was not evenly distributed across sectors; it was overwhelmingly driven by one. That observation is not a conclusion, but it is a signal. If aggregate stability rests on concentrated growth, then the question is no longer whether jobs were created, but why this particular sector is carrying the weight of the labor market at this moment.

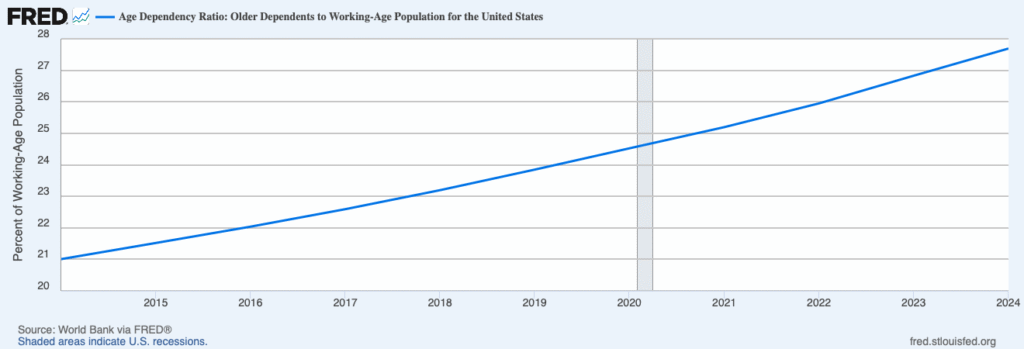

What the data ultimately reveals is not a labor market in recovery, but one in quiet transformation, a system whose surface stability conceals a deepening structural dependency on a single sector driven not by economic dynamism, but by demographic inevitability. When 137,000 jobs in private education and health services can simultaneously exceed the entire net nonfarm payroll gain and mask contraction across financial activities, information, and transportation, the headline number ceases to be a reliable measure of economic vitality. It becomes, instead, a statistical artifact, a figure that technically signals growth while the underlying composition whispers something more unsettling. The labor market is not expanding broadly; it is being held upright by the weight of an aging population that requires care, and by the workers, often underpaid, disproportionately female, and concentrated in non-tradable service roles, who provide it. Looking forward, the trajectory this data implies is not one of gradual normalization but of accelerating imbalance. As the Age Dependency Ratio continues its ascent, and the projections leave little ambiguity on that point, the working-age population will be asked to support an ever-larger share of older dependents while simultaneously filling the roles that serve them. This is not a temporary burden that productivity gains or immigration policy can easily offset; it is a structural compression of the labor force’s capacity to generate broad-based economic growth. If that pattern continues, what emerges is not a recession in the traditional sense, not a sharp contraction triggered by a demand shock or a credit event, but something more insidious: not only a slow-motion labor recession, but the early architecture of a collapse in the Pay-As-You-Go system that has quietly underwritten American retirement security for nearly a century.

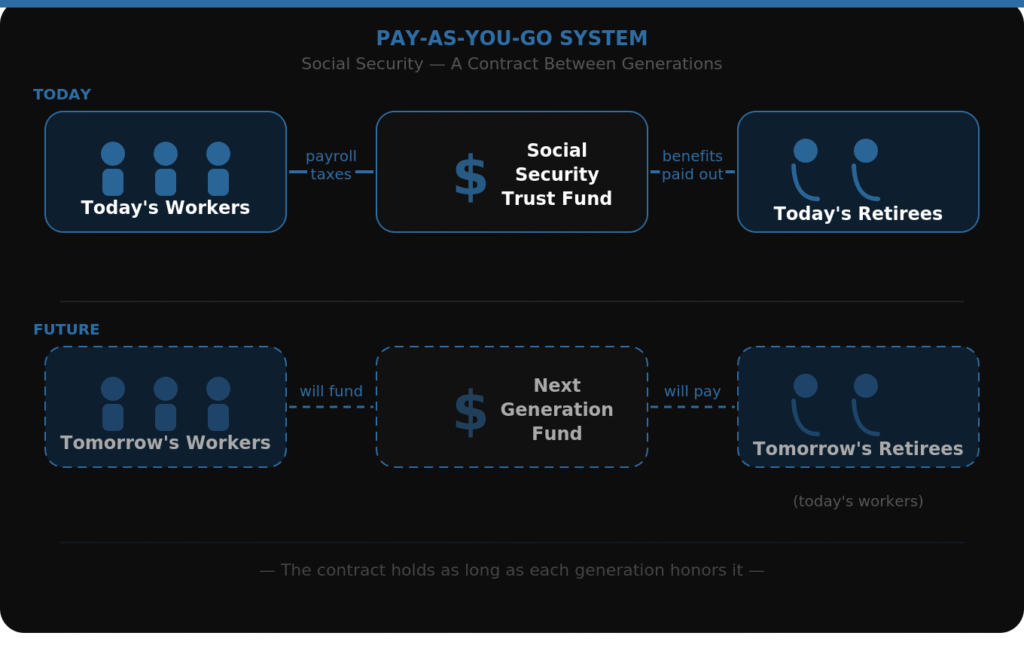

To understand why, one must understand the mechanical logic of Social Security itself. The system does not function as a personal savings account. It is not a vault where your contributions accumulate under your name, waiting for your retirement. It is, in its most precise description, a contract between generations: the workers of today fund the retirees of today, trusting that the workers of tomorrow will do the same for them.

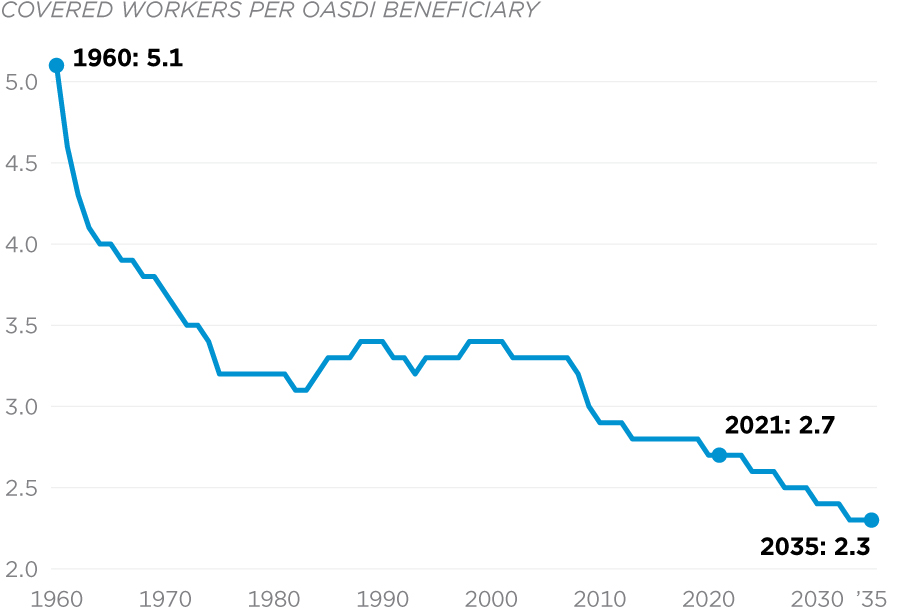

As the Age Dependency Ratio climbs from 21 to over 27 in less than a decade (image 2) the denominator of that intergenerational equation, the working-age population, shrinks in relative terms precisely as the numerator expands with the full force of Baby Boomer retirements, extended lifespans, and fertility rates hovering near 1.6. The Social Security Administration’s own projections estimate that the trust fund will be exhausted sometime between 2033 and 2035, at which point payroll tax revenues alone would cover only approximately 75 to 80 percent of promised benefits. And here lies the deepest tension in the January 2026 data: the sector that is single-handedly sustaining the headline employment number, care workers, home health aides, nursing staff, social assistance personnel, is also, by virtue of its characteristically lower wages, generating less payroll tax revenue per worker than the manufacturing, information, and financial sectors that are quietly contracting around it. The system is being asked to care for more people, with workers who contribute less to the fund designed to support those very people. That is not a policy failure in the conventional sense. It is a structural contradiction embedded in the demographic arithmetic itself.

Which brings us to a question that the data does not answer but that intellectual honesty demands we ask: who is going to pay for our Social Security? Not as a political provocation, but as a genuine analytical obligation, because if the labor market continues to concentrate its growth in lower-wage, demographically driven service roles while productive sectors stagnate, and if the working-age population continues to shrink relative to the dependent population it is asked to support, then the intergenerational contract at the heart of the Pay-As-You-Go system is not simply under pressure. It is being quietly renegotiated by forces that no single policy lever was designed to address. The Federal Reserve can adjust interest rates. Congress can debate benefit adjustments. But neither institution can reverse the arithmetic of an aging population, a declining birth rate, and a labor market whose growth is increasingly indistinguishable from the demographic crisis it is trying to manage. To read January 2026 as simply a month of modest but solid job growth is to mistake the surface for the structure. The surface holds. The structure is shifting, and it has been, steadily and without interruption, for a decade. The question is no longer whether we will feel it. The question is whether we will have the analytical clarity to see it before it becomes unavoidable.